Positioning for Uncertainty and Euphoria

Markets are priced for perfection. The fund is positioned for uncertainty.

Markets are priced for perfection. The fund is positioned for uncertainty.

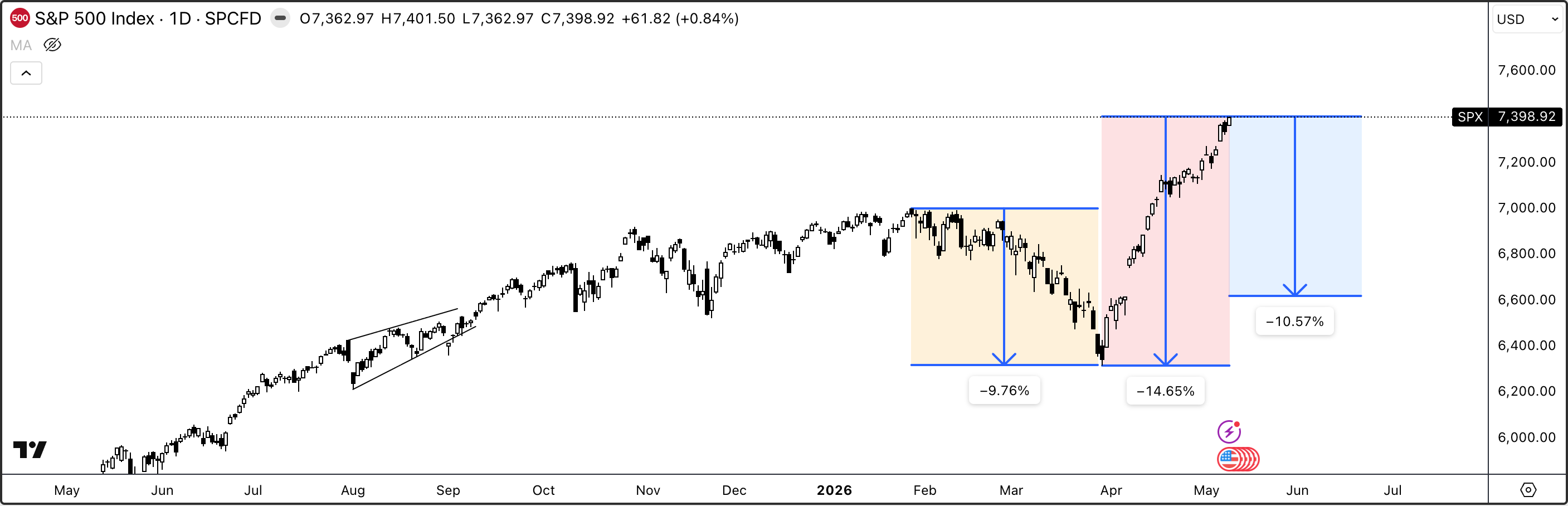

Current SPX put pricing through the next rebalance implies the market is assigning less than a 20% probability to a -10% drawdown on the S&P 500, and less than 15% to a retest of the war lows.

Three forces are shaping the road ahead: the euphoria in equities, the conflict in the Strait of Hormuz, and a possible inflation impulse. This note lays out the fund’s strategic and tactical response — across equities and fixed income — to each of them.

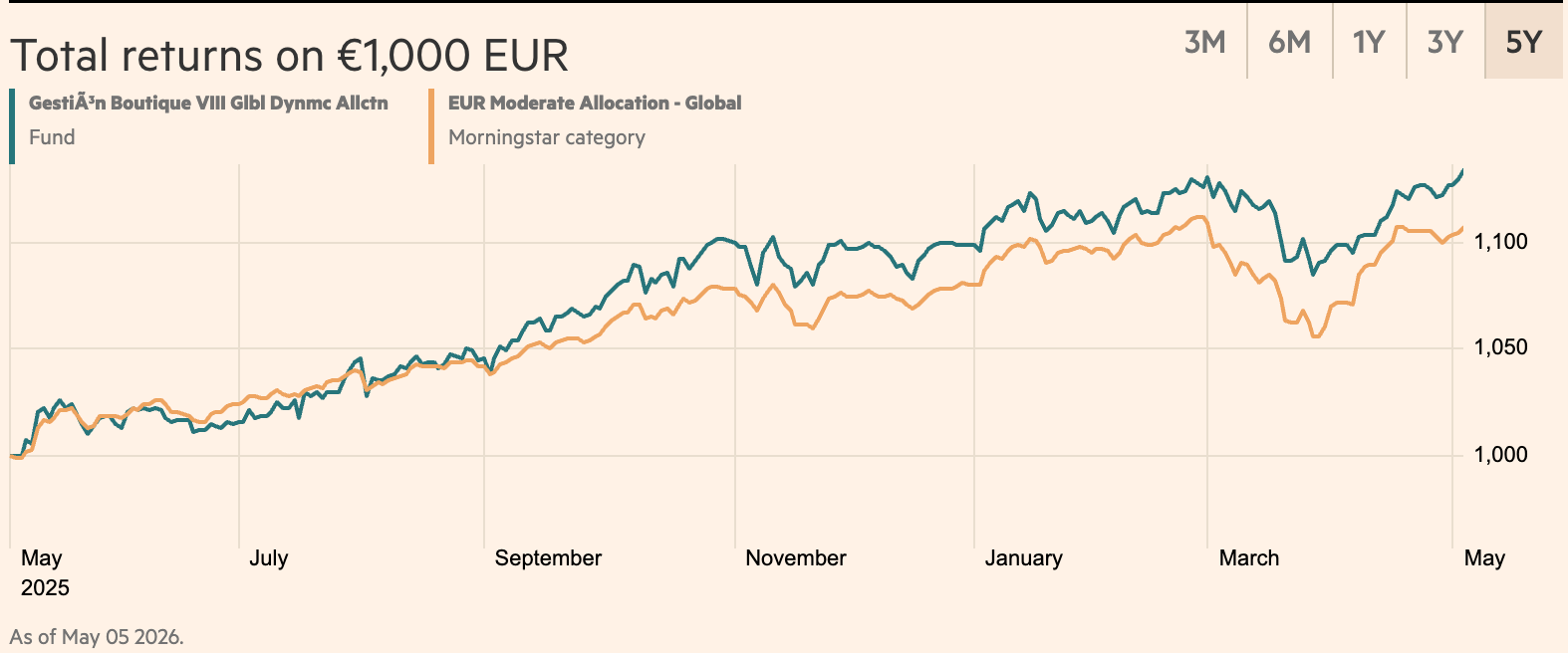

The global multi-asset macro fund implementing my research completed its first year of track record on May 5th — a year that included navigating the Trump tariffs and being correctly positioned through the Iran war via an overweight in energy.

First-year performance

Net return: +13.52% in EUR, +17.18% in USD

Volatility: 6.8%

Sharpe ratio: 1.7 (using the current 2% EUR risk-free rate)

Max drawdown: -4%

Given the fund’s capital-preservation mandate, current market-implied probabilities, and a conservative buffer, I’m working with the following base case through the next rebalance:

10% — Middle East conflict escalates

20% — Market re-prices a 2022-style high-inflation regime

70% — The 2023–present AI-boom regime continues

Every forecast and positioning decision in this note is probability-weighted across these three scenarios — covering equity sectors, regions, factors, and fixed income duration, currency, and credit quality.

Net of this rebalance, we expect the portfolio to deliver +1.83% over the next three months — 74 bps above our benchmark (3% annualized), with only 5 bps of additional volatility and materially better tail-risk management.

Below: the strategic and tactical overweights driving the 74 bps of expected alpha, the duration and credit-quality calls in fixed income, and how the 30% non-base-case tail is hedged.